Imagine a technology that could preserve our freedoms for future generations, redeem the liberation for sensitive folks, and transform the world as we know it. Imagine no more! Because blockchain is such a technology and breakthrough in database technology that makes it happen.

Blockchains allow the development of applications where multiple parties can record digital transactions without needing a trusted or central authority (like international currency transactions). Such an approach has profound implications for election integrity, securities settlement, duplicate medical records, and music distribution.

So, even if you're a total newbie, you'll find the information herein beneficial. It's all boiled down in a very easy-to-understand format; even the greenest of beginners will find it easy to work with.

This comprehensive guide introduces you to the following topics concerning blockchain technology

- What is blockchain technology?

- How does blockchain technology work?

- Types of blockchains

- Need for blockchain technology

- Problems solved by blockchain technology and its applications

- Main pillars of blockchain technology

- Does blockchain mean the end of SWIFT ?

- Benefits of blockchain technology

- Future of blockchain technology

- When is blockchain tech a good fit for your business?

What is Blockchain Technology?

A blockchain is only a type of database. It is a concept that seems complicated, but if understood, it's pretty simple.

Here in 'blockchain,' the block means a piece of information, i.e., data, and chain refers to - information/data blocks bound using cryptographic principles.

Remember, these data blocks are immutable/unchangeable.

Blockchain is governed by a cluster of computers located around the globe. hey are neither owned nor managed by any single entity at all costs. Hence, all data blocks are secured, and no one can alter their info, making this technology the most secure and advanced structure of financial transactions and data sharing.

How does Blockchain Technology Work?

Blockchain technology aims to allow the flow of digital information without being altered.

Hence, the foundation of time-stamped immutable ledgers or records of transactions that cannot be altered, deleted or destroyed. Isn't this what people want?

And because of this characteristic of blockchains, blockchain is a revolutionary technology in its rights and is also known as distributed ledger technology (DLT), permissioned ledger technology, etc. - they all found their roots in critical concepts for the development of Bitcoin at the beginning of the year 2008. The common thread among them is that they decentralize trust,

making blockchain more demanding and futuristic.

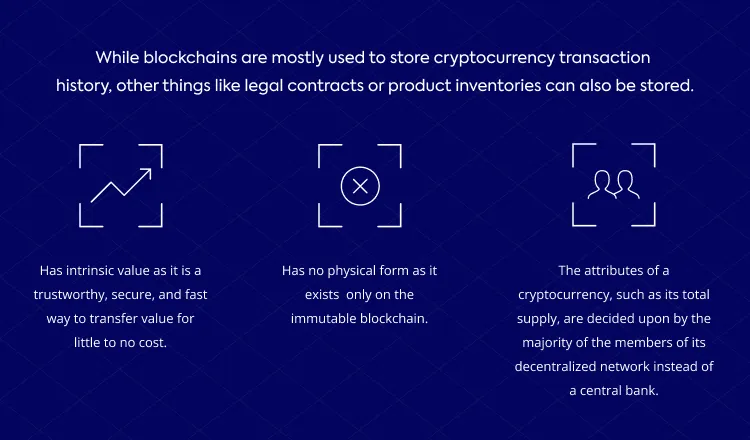

Blockchains are shared immutable databases, meaning each concerning party has access to the complete data and its entire history. No single party is allowed to control the information and its flow.

Using blockchain technology, every party can verify each transaction against its copy of the blockchain. Thus, it is nearly impossible for hackers or anyone to forge records or info.

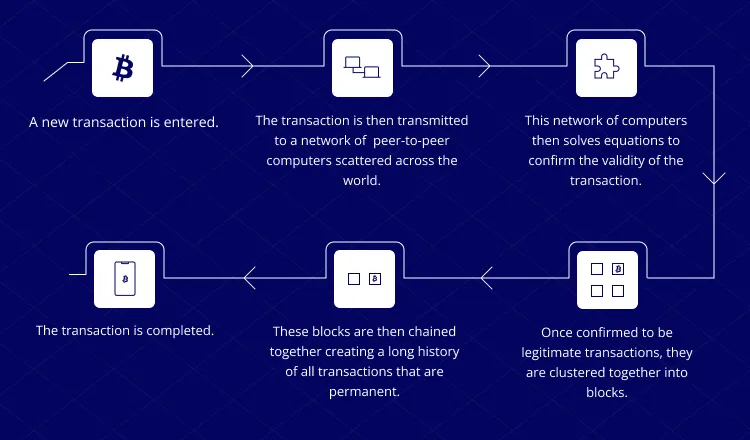

Transaction process

In blockchain-based technology, the process of transaction is immediate and permanent. The transaction also leaves its footprints on each node across the system. Every transaction detail, like a price, ownership, asset, etc., is recorded in a blockchain within seconds.

And any alterations made in one ledger prompt the others to register automatically. It eliminates the possibility of the involvement of any third- party verification since every transaction is a trustworthy system without third-party validation. This futuristic technology suits transaction involving assets, goods, money, or content.

Types of blockchains

There are mainly four types of blockchain networks:

1. Public Blockchain

This type of blockchain is a non-restrictive distributed ledger; anyone with internet access can sign in to become an authorized node.

Use For mining and exchanging cryptocurrencies.

, For Example, - Bitcoin, Ethereum, and Litecoin.

Note: You need to follow security protocols using a public blockchain.

2. Private Blockchain

The private type of blockchain is a restrictive ledger operating in a closed network. Private organizations use private blockchains with restricted access. And mostly, only chosen members are part of this type of blockchain. The member organization controls its security, permissions, and accessibility.

Use - For voting, digital identity, ownership of assets, etc.

3. Consortium Blockchain

It is a type of semi-decentralized network of blockchain managed by more than one organization. Several organizations have access to this network or can exchange info as well.

Used by Banks, Govt. Organizations and similar institutions.

4. Hybrid Blockchain

This type of blockchain network is an amalgamation of a private and a public blockchain. It can use features of both private and public blockchain networks.

Note: This type of blockchain network has a flexible node in which information can be discrete or kept open depending on an individual's choice.

Need for Blockchain Technology

Remember the miserable financial crisis of 2008? If not, search it over YouTube or Google to find enormous info. During this period, a person, or a group of people, pseudonymized as Satoshi Nakamoto, realized the terror of the centralized financial system.

We all have centralized financial systems governed by national governments and

are sensitive to happenings in the Global Market.

In a centralized system, whenever one needs to send money to one location/country or even commits a simple transaction, it must get help from a third party, such as a bank or escrow services like PayPal.

Such centralized third parties have tremendous power in their hands.

For example -

- All your info is with them.

- They can freeze your account. For this, you can think of international sanctions on a country.

- You have no other way than to trust the current financial system.

Hence, in the light of such drawbacks of a centralized financial system, Satoshi Nakamoto suggested having a decentralized and peer-to-peer financial system that involves a digital currency or, say, a cryptocurrency called Bitcoin.

Note: Blockchain technology is the basis for Bitcoins.

Problems are solved by Blockchain Technology and its Applications.

The centralized financial system has many drawbacks and the one that is eating it is the double spending problem , which has plagued it since its inception. But blockchain technology is a breakthrough invention and is so revolutionary that it can change how we deal with money and other financial entities.

A digital currency like Bitcoin is similar to any computer file, containing some 0s and 1s. And you might think it would be easy for anyone to counterfeit it just by a simple copy-and-paste mechanism. But it's not so!

Because before blockchain technology, banks used to keep track of banknotes in everyone's bank account so that no one could use them twice. But what the blockchain does differently is that it makes these ledgers or transaction books public, making it easy for everybody to verify that no one is using the same coin/note twice.

Besides that, the concept of blockchain technology eliminates the ntermediaries involved because there is no need for a third party (like a bank or services like PayPal) to manage accounts and transactions since it directly executes trades by connecting affiliated peers.

It has the following benefits:

- Faster and cheaper transactions. What can be better than that? Right?

- Your info is now more private since banks are not involved. Awesome!

Isn't it what people are waiting for?

Now, you are beginning to see its importance.

Blockchain Technology Applications

Blockchain has recently become synonymous with Bitcoin and cryptocurrency. However, its applications and use cases go beyond financial transactions. Companies in every industry are beginning to understand applying blockchain-based solutions to solve business problems.

The sectors in which blockchain is making its robust contributions are -

Use of Blockchain in Content Distribution

The licenses for creating media content and its distribution are sold country by country. And subscribers/users struggle to access the content in another country. Blockchain technology's immutability and transparency feature enables content creators and their distributors to manage content peer-to-peer.

Hence, making it easy for users to subscribe to the content leaves no space for piracy or duplicity. It will benefit original content creators directly, and blockchain will revolutionize this industry.

Blockchain in Real-Estate and Agriculture

Blockchain technology is finding its many use cases in the real estate sector. And because of its immutable distributed ledger feature, its positive effects continue to become more evident.

Blockchain can help tenants, landlords, estate agents, and even architects securely buy, sell, rent, or lease property in real estate. This technology can quickly solve many legal complications and administrative hurdles. An abundance of opportunities lies ahead in this field.

Another sector that will benefit from this technology - is the agriculture and food industry. Based on a survey by Forbes , blockchain technology is all set to revolutionize the food industry, making it easy for organizations to trace the path and safety of food, right from farms to the buyer.

For example, IBM's Food Trust Blockchain . It is one of the most successful implementations of blockchain technology in the food industry.

Blockchain Technology in the Travel Industry

Do you ever wonder about your data's security during your travel journey? It's believed that blockchain's capabilities can transform it into real-time travel experiences with no compromise in the security of any data because blockchain's features work like a security wrapper that creates an entirely different way of sharing and managing information related to airlines via a secure and authorized access requirement.

Blockchain is a game-changer for online advertising and the entertainment industry.

Today, the digital medium of consuming information is at its peak and has changed the world as we perceive it. The same goes for consumers, artists, and brands. And the United States economy loses a net $12.5 billion yearly from online music theft.

Besides that, the potential for fraud has jumped to a growth rate of 19% annually. And all that in account, online advertising fraud costs companies about $19 billion annually.

Thus, with the help of blockchain tech, in the travel and tourism, people could directly pay authors and artists without needing a record label or third-party firm handling them.

Blockchain in the Energy Sector

Today, the clean and sustainable energy conversation is heating like never before. Major energy providers across the globe use cheap, unsustainable, coal-based energy production. Blockchain can help produce energy generation efficiently using cryptocurrency mining.

Moreover, people can use blockchain technology to monitor gas and electricity expenditure using smart meters that provide real-time information to simplify energy bills. It will be painless since blockchain will make bills and accounts immutable, leaving no room for fraud or misuse.

Healthcare and Education Sectors are Shifting toward Blockchain.

Blockchain technology in the healthcare sector can find many use cases, , for example, - storing and managing patients' medical records. Because the very definition of blockchain states this is an immutable digital ledger, hence no case of data tampering! And no room for even a single point of fraud. Isn't that amazing? Sure, it is the best tech for people's privacy!

Another sector wherein blockchain's capabilities can hugely benefit is the education industry.

For example, Managing massive student records - attendance, grades, course material, graduation certificates, etc.

Thus, blockchain's collaborative implementation will streamline a lot of things.

Blockchain is Revolutionizing the Banking and Finance Sector.

Blockchain technology is disrupting the Fintech and banking industry. Both sectors have benefitted post-integration. There is a surge in the trust factor and efficiency of business operations. Blockchain is helping to reduce the time for transactions and associated charges and securing and storing customer data at low-cost solutions.

An old report in 2016 from Capgemini states; that consumers could pay at least $16 billion in insurance and banking charges every year via blockchain-based software applications. And the global investment value in the Fintech industry alone rose from approx—$3 billion in 2013 to $8 billion in 2018.

Main Pillars of Blockchain Technology

There are mainly three pillars of blockchain technology -

Decentralization

Since the centralized financial market has many loopholes and drawbacks, decentralization is the foundation stone of blockchain technology. Decentralization gives flexibility to the entire blockchain network.

With blockchains, information isn't owned by an individual or an organization; instead, it is owned by each network member. This eliminates any need for a third party and has made financial transactions very easy, allowing money-related secure transactions anywhere without visiting or involving a bank.

For example, Bitcoins are a digital currency that thrives on this concept.

Transparency

Besides decentralization is one of the main features of blockchain technology, transparency is another. Blockchain allows access to all transactions, making financial transactions convenient since the records are recorded in the database, which is open to anyone.

Immutability

Immutability is one of the crucial features of blockchain; it means something that cannot be altered/changed.

In case of financial fraud and data tampering in financial institutions, this booming feature of blockchain prevents all kinds of illegal activities. In a blockchain, this feature is introduced using the cryptographic hash function (a mathematical algorithm for mapping data).

Now, you might think, what is hashing?

Hashing refers to a process wherein the input is a string of any length in a system, and the output is of a fixed length.

Does blockchain mean the end of SWIFT?

First, let's get to know what SWIFT stands for. Its complete form is - Society for Worldwide Interbank Financial Telecommunication. It is a consortium of banks that manages a bulk of global transactions.

You might already know SWIFT or have heard of it because of the Russia-Ukraine ongoing instability in the geopolitical relationship. SWIFT's messaging system allows interbank transfers globally. And these cross-border money transfers are essential to today's global banking system, which amounted to USD 150 T in 2015.

Anyway, is the introduction of blockchain is the end of SWIFT?

Well!, we're not there yet! But with blockchain's distributed ledger and its ability to allow transactions with minimal fees, blockchain can disrupt the cross-border fund transfer systems in unimaginable ways, posing a significant threat to SWIFT.

And there are reports that the share of messages related to transactions within the SWIFT ecosystem has notably declined. But traction for SWIFT's new product and increase in revenue from alternate streams suggests that SWIFT might be reinventing itself instead of becoming obsolete in a blockchain world.

Benefits of Blockchain Technology

Apart from the many benefits that blockchain technology brings with it, below are the ones that make industry leaders go for it:

Robust security

In blockchains, data is highly secured using cryptographic keys. Plus, blockchain networks are pretty resilient to cyber-attacks and data tampering.

Faster transactions at cheaper costs -

Since technology takes care of this, there is no need for traditional third parties like banks and lawyers to authenticate transactions. And it's suitable for businesses to streamline their processes at reduced costs.

Excellent transparency and traceability -

Blockchain is unique for transparency and traceability of info that flows before every network member in its database. Blockchain allows access to the entire database related to transactions and their history. As a result, users benefit from real-time transaction-level assurance.

Future of blockchain technology

Blockchain is opening doors to new business ways and predicting promising future growth. Insights from Gartner report:

- If you have already established at least one innovative business that runs on blockchain technology, it will be worth nearly $10 billion by 2022, i.e., this year.

- And blockchain will add a business value of over $360 billion by 2026, growing to more than $3.1 trillion by 2030.

The concept of blockchain has far-reaching applications. It has many breakthroughs across various economic sectors - NFTs and digital currency and transactions being its focus in present scenarios.

Blockchain's industrial functions involve:

- Deployment to facilitate identity management.

- Supply chain analysis.

- Smart contracts, and many more.

Blockchain technology will be transformative in ways we have never imagined; from the tech and IT sector to healthcare and education, it has the potential to revolutionize many industries within a few years.

When is Blockchain Tech a good fit for your Business?

One of the Harvard Review Reports points out the truth about blockchain development services are now emerging and hype in future. Blockchain technology is complex and needs prior research and thoughtfulness about integrating it into the current operations and technology stacks.

Enterprises and businesses seeking to use its considerable strengths need first to ensure that they clearly understand the business problem that they want to address and whether blockchain technology is the right step forward; as Shira Rubinoff, the President of Prime Tech Partners mentions

Companies do not need to understand precisely what problem they are looking to solve and whether blockchain is the right vehicle to get it done .

Moreover, quality and security are foundational to blockchain technology. Thus, companies need to ask a simple question - whether it would help or hinder business objectives.

Because the research report from SalesForce shows that over 22% of global IT leaders have already found a use case for blockchain technology and mapped its capabilities in their business operations. They aren't wasting any time, meaning they have already started working on blockchain projects.

When are you going to use blockchain in your firm? Because at present, blockchain technology is set to disrupt healthcare records management, voter fraud, distribution of welfare, and many more sectors of the world economy.

Tags

Blockchain app development

blockchain technology

Blockchain

Blockchain development